How Mortgage Rate Changes Impact Your Homebuying Power

How Mortgage Rate Changes Impact Your Homebuying Power If you’re thinking about buying or selling a home, you’ve probably got mortgage rates on your mind. That’s because you’ve likely heard that mortgage rates impact how much you can afford in your monthly mortgage payment, and you want to factor th

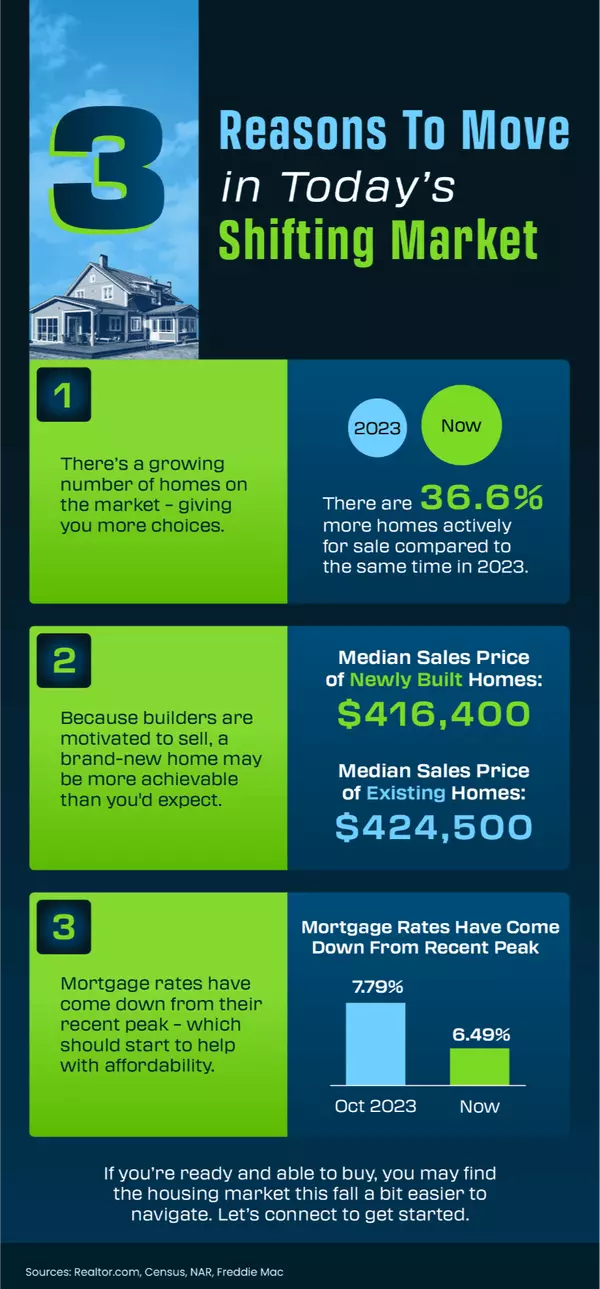

3 Reasons To Move in Today’s Shifting Market

What Credit Score Do You Really Need To Buy a House?

What Credit Score Do You Really Need To Buy a House? When you're thinking about buying a home, your credit score is one of the biggest pieces of the puzzle. Think of it like your financial report card that lenders look at when trying to figure out if you qualify, and which home loan will work best f

Recent Posts